The Old Routine: More Fees, Less Value

You've done the hard part. You've saved, invested, and built a portfolio worth a few hundred thousand dollars — maybe more. But then life happens. You need $100K for a renovation, a business opportunity, a bridge loan, or a tax bill. Whatever the reason, you've got the assets; you just need the cash.

So you look at your options:

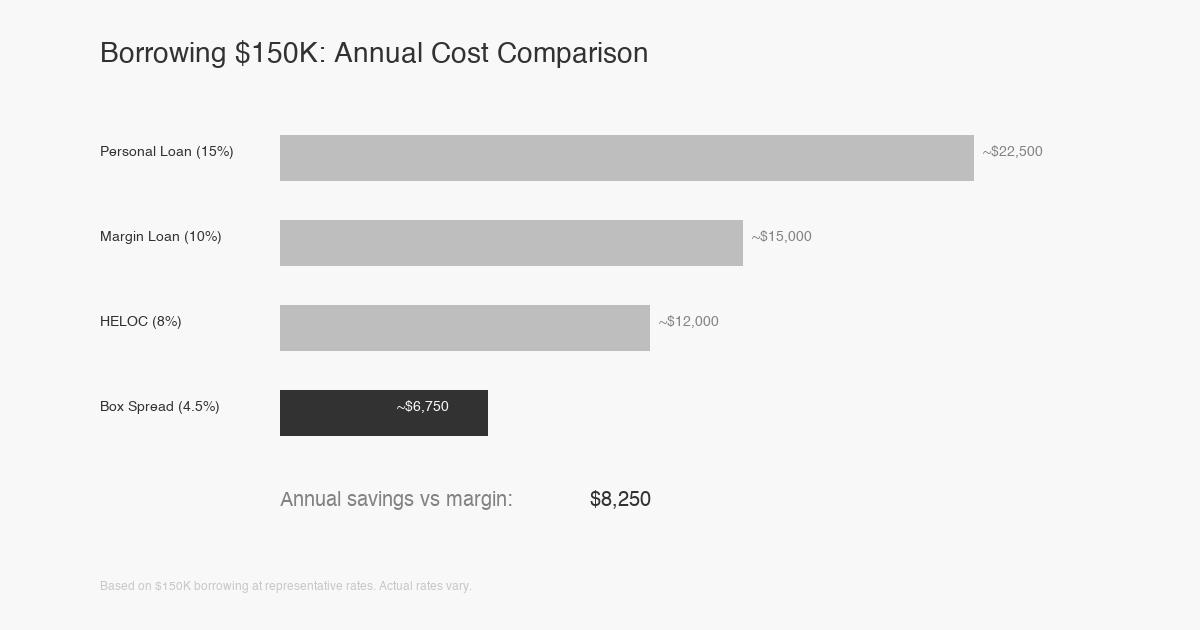

- Sell investments? Capital gains tax could immediately consume 15-23.8% of your profit. A $100K sale with a low cost basis could cost you over $20,000 in taxes before you've spent a dollar.

- Margin loan? Your brokerage demands 8-13% annually. On $100K, that's $8,000-$13,000 a year in interest. For money you already have — it's just in the wrong form.

- HELOC? 7-9%, plus paperwork, appraisals, and your house as collateral.

- Personal loan? Don't even look. It's 10-24%.

The Box Spread: Your Secret Weapon

There's a fourth option most people never hear about, yet institutions have been utilizing it for decades. Enter the Box Spread.

A box spread is an options strategy that acts like a self-constructed loan. No bank, no application, no credit check. You use index options to lock in a guaranteed payoff at a future date, and the difference between what you pay today and what you collect later is your borrowing cost.

The rate? Typically near Treasury yields — currently about 4-5%.

Read that again. 4-5%. While your brokerage charges you 10% or more for margin. That gap — the 5-6% difference — isn't a rounding error on a $200K loan. It's $10,000-$12,000 a year you're handing over to your broker unnecessarily.

How It Works (Without the Math Degree)

A box spread combines four options positions on a broad index like the S&P 500 (SPX). When structured correctly, the outcome is predetermined — it doesn't matter whether the market rises, falls, or remains flat. You receive a fixed dollar amount at expiration.

Think of it as purchasing a Treasury bill, but through the options market. You pay $95,500 today. In one year, you receive $100,000. Guaranteed. This translates to a 4.7% implied rate.

The "loan" is the cash you receive upfront. The "repayment" occurs automatically at expiration when the options settle. There are no monthly payments, no loan officer, and no underwriting. Just math.

Why This Matters for the Mass Affluent

If you have $250K to $2M in investable assets, you're in a uniquely frustrating position. You're wealthy enough to need sophisticated financial tools but are often stuck with retail pricing. Box spreads alter this equation significantly in three ways:

- Borrow at Institutional Rates: Box spreads eliminate the markup associated with margin loans, potentially saving you thousands annually.

- Avoid Triggering Capital Gains: Access liquidity without selling a single share, maintaining your portfolio's long-term growth potential.

- Favorable Tax Treatment: Benefit from the 60/40 Rule and potential investment interest deductions.

A Practical Example

Consider Sarah, who has a $750K portfolio and needs $150,000 for a down payment on a rental property. Selling stock would trigger over $30,000 in capital gains taxes.

Instead, she opens box spreads on SPX options with a one-year expiration:

- Borrows: $150,000 via box spreads

- Implied rate: 4.6%

- Annual cost: $6,900

- Tax saved by not selling: $30,000+

She keeps her portfolio intact, obtains her liquidity, acquires the rental property, and her total borrowing cost is less than a quarter of what she would have paid in capital gains taxes alone.

The Risks (Because Every Edge Has One)

- Margin requirements can change. Brokers can increase collateral requirements, potentially forcing you to add cash or close positions at an inconvenient time.

- You're rate-locked. If rates drop significantly after you open a box spread, you're committed until expiration (though you can close early at market prices).

- Execution complexity. Four simultaneous options legs require precision. Use a broker with good multi-leg order types and tight SPX spreads.

Why Now?

Two trends are converging:

- Falling rates make box spread borrowing cheaper in absolute terms. A 4% implied rate is significantly different from the 6%+ rates of 2023-2024.

- Rising portfolios mean more people are sitting on larger unrealized gains. The mass affluent are wealthier than ever on paper, and the tax cost of accessing that wealth through selling has never been higher.

You wouldn't pay full price for a car without investigating what dealers are actually selling for. So why pay full price for borrowing when there's a wholesale alternative available right in your options chain?

Box spreads aren't exotic. They aren't risky in the way options are often imagined to be. They're a fixed-income instrument disguised as an options trade — and they offer mass affluent investors the same borrowing economics institutional money has enjoyed for decades.

Lower rates. Tax efficiency. No forced liquidation. Consider having a conversation with your advisor or CPA. It might be worth exploring a more efficient way to access your own wealth.